1 Introduction

In previous publications I have covered regression models from the scikit-learn library and the statsmodel library. But besides these, there are a lot of other machine learning algorithms that can be used to create regression models. In this publication I would like to introduce them to you.

Short remark in advance: I will not go into the exact functioning of the different algorithms below. In the end I have provided a number of links to further publications of mine in which I explain the algorithms used in detail.

For this post the dataset House Sales in King County, USA from the statistic platform “Kaggle” was used. You can download it from my GitHub Repository.

The goal is to find an algorithm that can best predict house prices. The results of the algorithms will be stored in variables and presented in an overview at the end.

2 Loading the libraries and the data

import pandas as pd

import numpy as np

from sklearn.model_selection import train_test_split

import matplotlib.pyplot as plt

from sklearn import metrics

from sklearn.metrics import accuracy_score

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import GridSearchCV

from sklearn.model_selection import RandomizedSearchCV

from sklearn.linear_model import LinearRegression

from sklearn.tree import DecisionTreeRegressor

from sklearn.svm import SVR

from sklearn.linear_model import SGDRegressor

from sklearn.neighbors import KNeighborsRegressor

from sklearn.ensemble import BaggingRegressor

from sklearn.ensemble import RandomForestRegressor

from sklearn.ensemble import AdaBoostRegressor

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.ensemble import StackingRegressor

from sklearn.linear_model import Lasso

from sklearn.linear_model import Ridgehouse = pd.read_csv("path/to/file/house_prices.csv")house = house.drop(['zipcode', 'lat', 'long', 'date', 'id'], axis=1)

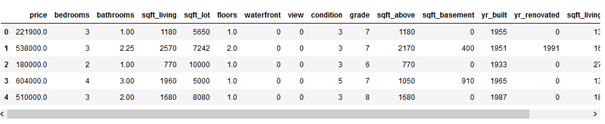

house.head()

x = house.drop('price', axis=1)

y = house['price']

trainX, testX, trainY, testY = train_test_split(x, y, test_size = 0.2)3 Linear Regression

lm = LinearRegression()

lm.fit(trainX, trainY)

y_pred = lm.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_lm = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_lm = lm.score(trainX, trainY)4 Decision Tree Regression

dt_reg = DecisionTreeRegressor()

dt_reg.fit(trainX, trainY)

y_pred = dt_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_dt_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_dt_reg = dt_reg.score(trainX, trainY)param_grid = {"criterion": ["mse", "mae"],

"min_samples_split": [10, 20, 40],

"max_depth": [2, 6, 8],

"min_samples_leaf": [20, 40, 100],

"max_leaf_nodes": [5, 20, 100],

}grid_dt_reg = GridSearchCV(dt_reg, param_grid, cv=5, n_jobs = -1) grid_dt_reg.fit(trainX, trainY)print(grid_dt_reg.best_params_)

y_pred = grid_dt_reg.predict(testX)

print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_grid_dt_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_grid_dt_reg = grid_dt_reg.score(trainX, trainY)5 Support Vector Machines Regression

svr = SVR(kernel='rbf')

svr.fit(trainX, trainY)

y_pred = svr.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_svr = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_svr = svr.score(trainX, trainY)k = ['rbf']

c = [0.001, 0.10, 0.1, 10, 25, 50, 100, 1000]

g = [1, 0.1, 0.01, 0.001, 0.0001, 0.00001]

param_grid=dict(kernel=k, C=c, gamma=g)grid_svr = GridSearchCV(svr, param_grid, cv=5, n_jobs = -1)

grid_svr.fit(trainX, trainY)print(grid_svr.best_params_)

y_pred = grid_svr.predict(testX)

print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_grid_svr = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_grid_svr = grid_svr.score(trainX, trainY)6 Stochastic Gradient Descent (SGD) Regression

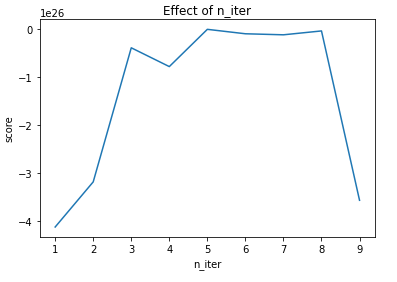

n_iters = list(range(1,10,1))

scores = []

for n_iter in n_iters:

sgd_reg = SGDRegressor(max_iter=n_iter)

sgd_reg.fit(trainX, trainY)

scores.append(sgd_reg.score(testX, testY))

plt.title("Effect of n_iter")

plt.xlabel("n_iter")

plt.ylabel("score")

plt.plot(n_iters, scores)

n_iter=5

sgd_reg = SGDRegressor(max_iter=n_iter)

sgd_reg.fit(trainX, trainY)

y_pred = sgd_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_sgd_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_sgd_reg = sgd_reg.score(trainX, trainY)params = {"alpha" : [0.0001, 0.001, 0.01, 0.1],

"penalty" : ["l2", "l1", "elasticnet", "none"],

}grid_sgd_reg = GridSearchCV(sgd_reg, param_grid=params, cv=5, n_jobs = -1)

grid_sgd_reg.fit(trainX, trainY)print(grid_sgd_reg.best_params_)

y_pred = grid_sgd_reg.predict(testX)

print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_grid_sgd_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_grid_sgd_reg = grid_sgd_reg.score(trainX, trainY)7 KNN Regression

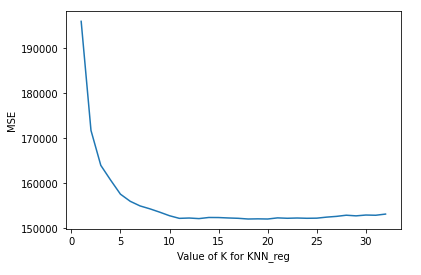

k_range = range(1, 33)

scores = {}

scores_list = []

k_range = range(1, 33)

scores = {}

scores_list = []

for k in k_range:

knn_reg = KNeighborsRegressor(n_neighbors=k)

knn_reg.fit(trainX, trainY)

y_pred = knn_reg.predict(testX)

scores[k] = metrics.mean_absolute_error(testY, y_pred)

scores_list.append(metrics.mean_absolute_error(testY, y_pred))plt.plot(k_range, scores_list)

plt.xlabel('Value of K for KNN_reg')

plt.ylabel('MSE')

n_eighbors = 16

knn_reg = KNeighborsRegressor(n_neighbors=n_eighbors)

knn_reg.fit(trainX, trainY)

y_pred = knn_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_knn_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_knn_reg = knn_reg.score(trainX, trainY)k_range = list(range(1,15))

weight_options = ["uniform", "distance"]

params = dict(n_neighbors=k_range, weights=weight_options)grid_knn_reg = GridSearchCV(knn_reg, param_grid=params, cv=5, n_jobs = -1)

grid_knn_reg.fit(trainX, trainY)print(grid_knn_reg.best_params_)

y_pred = grid_knn_reg.predict(testX)

print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_grid_knn_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_grid_knn_reg = grid_knn_reg.score(trainX, trainY)8 Ensemble Modeling

I’ll define a function that returns the cross-validation RMSE error so we can evaluate our models and pick the best tuning part.

def rmse_cv(model):

rmse= np.sqrt(-cross_val_score(model, trainX, trainY, scoring="neg_mean_squared_error", cv = 5))

return(rmse)8.1 Bagging Regressor

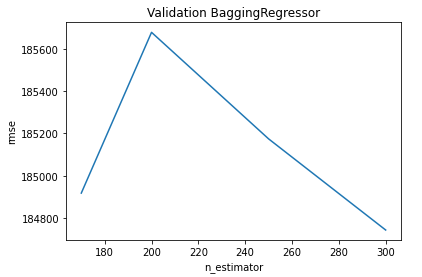

n_estimators = [170, 200, 250, 300]

cv_rmse_br = [rmse_cv(BaggingRegressor(n_estimators = n_estimator)).mean()

for n_estimator in n_estimators]cv_br = pd.Series(cv_rmse_br , index = n_estimators)

cv_br.plot(title = "Validation BaggingRegressor")

plt.xlabel("n_estimator")

plt.ylabel("rmse")

cv_br.min()

n_estimators = 300

bagging_reg = BaggingRegressor(n_estimators = n_estimators)

bagging_reg.fit(trainX, trainY)

y_pred = bagging_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_bagging_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_bagging_reg = bagging_reg.score(trainX, trainY)8.2 Bagging Regressor with Decision Tree Reg as base_estimator

As the base estimator I’ll use a DecisionTreeRegressor with the best parameters calculated with grid search under chapter 4.

dt_reg_with_grid_params = DecisionTreeRegressor(criterion = 'mse', max_depth= 8, max_leaf_nodes= 100, min_samples_leaf= 20, min_samples_split= 10) n_estimators = 250

bc_params = {

'base_estimator': dt_reg_with_grid_params,

'n_estimators': n_estimators

}bagging_reg_plus_dtr = BaggingRegressor(**bc_params)

bagging_reg_plus_dtr.fit(trainX, trainY)

y_pred = bagging_reg_plus_dtr.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_bagging_reg_plus_dtr = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_bagging_reg_plus_dtr = bagging_reg_plus_dtr.score(trainX, trainY)8.3 Random Forest Regressor

n_estimators = 250

rf_reg = RandomForestRegressor(n_estimators = n_estimators)

rf_reg.fit(trainX, trainY)

y_pred = rf_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_rf_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_rf_reg = rf_reg.score(trainX, trainY)param_dist = {"max_depth": list(range(3,20)),

"max_features": list(range(1, 10)),

"min_samples_split": list(range(2, 11)),

"bootstrap": [True, False],

"criterion": ["mse", "mae"]}n_iter_search = 10

rs_rf_reg = RandomizedSearchCV(rf_reg, param_distributions=param_dist,

n_iter=n_iter_search, n_jobs = -1)

rs_rf_reg.fit(trainX, trainY)print(rs_rf_reg.best_params_)

y_pred = rs_rf_reg.predict(testX)

print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_rs_rf_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_rs_rf_reg = rs_rf_reg.score(trainX, trainY)8.4 AdaBoost Regressor

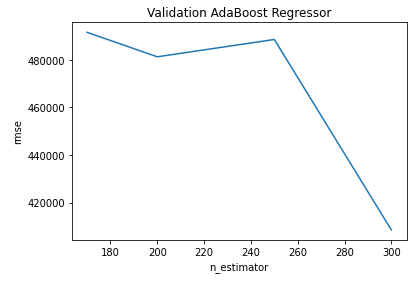

n_estimators = [170, 200, 250, 300]

cv_rmse_ab_reg = [rmse_cv(AdaBoostRegressor(n_estimators = n_estimator)).mean()

for n_estimator in n_estimators]cv_ab_reg = pd.Series(cv_rmse_ab_reg , index = n_estimators)

cv_ab_reg.plot(title = "Validation AdaBoost Regressor")

plt.xlabel("n_estimator")

plt.ylabel("rmse")

cv_ab_reg.min()

n_estimators = 300

ab_reg = AdaBoostRegressor(n_estimators = n_estimators)

ab_reg.fit(trainX, trainY)

y_pred = ab_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_ab_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_ab_reg = ab_reg.score(trainX, trainY)8.5 AdaBoost Regressor with Decision Tree Reg as base_estimator

I will use again the DecisionTreeRegressor with the best parameters calculated with grid search under chapter 4.

dt_reg_with_grid_params = DecisionTreeRegressor(criterion = 'mse', max_depth= 8, max_leaf_nodes= 100, min_samples_leaf= 20, min_samples_split= 10) n_estimators = 300

ab_params = {

'n_estimators': n_estimators,

'base_estimator': dt_reg_with_grid_params

}ab_reg_plus_dtr = AdaBoostRegressor(**ab_params)

ab_reg_plus_dtr.fit(trainX, trainY)

y_pred = ab_reg_plus_dtr.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_ab_reg_plus_dtr = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_ab_reg_plus_dtr = ab_reg_plus_dtr.score(trainX, trainY)8.6 Gradient Boosting Regressor

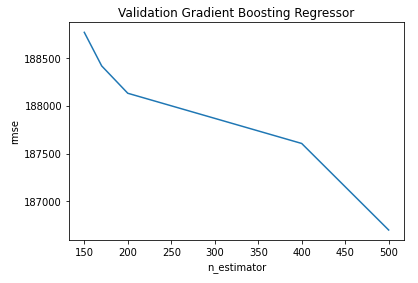

n_estimators = [150, 170 , 200, 400, 500]

cv_rmse_gb_reg = [rmse_cv(GradientBoostingRegressor(n_estimators = n_estimator)).mean()

for n_estimator in n_estimators]cv_gb_reg = pd.Series(cv_rmse_gb_reg , index = n_estimators)

cv_gb_reg.plot(title = "Validation Gradient Boosting Regressor")

plt.xlabel("n_estimator")

plt.ylabel("rmse")

cv_gb_reg.min()

n_estimators = 500

gb_reg = GradientBoostingRegressor(n_estimators = n_estimators)

gb_reg.fit(trainX, trainY)

y_pred = gb_reg.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_gb_reg = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_gb_reg = gb_reg.score(trainX, trainY)8.7 Stacking Regressor

ridge = Ridge()

lasso = Lasso()estimators = [

('ridge', Ridge()),

('lasso', Lasso())]sr = StackingRegressor(estimators=estimators, final_estimator=LinearRegression())

sr.fit(trainX, trainY)

y_pred = sr.predict(testX)print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_sr = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_sr = sr.score(trainX, trainY)params = {'lasso__alpha': [x*5.0 for x in range(1, 10)],

'ridge__alpha': [x/5.0 for x in range(1, 10)]}grid_sr = GridSearchCV(sr, param_grid=params, cv=5)

grid_sr.fit(trainX, trainY)print(grid_sr.best_params_)

y_pred = grid_sr.predict(testX)

print('Mean Absolute Error:', round(metrics.mean_absolute_error(testY, y_pred), 2))

mae_grid_sr = round(metrics.mean_absolute_error(testY, y_pred), 2)

r_grid_sr = grid_sr.score(trainX, trainY)9 Overview Results

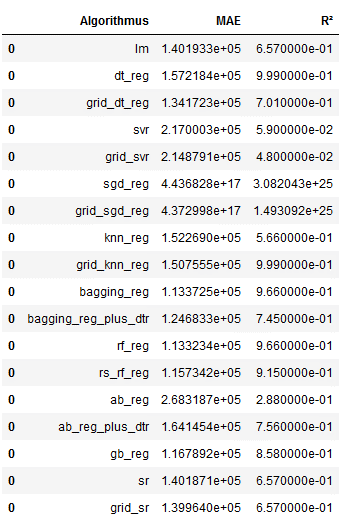

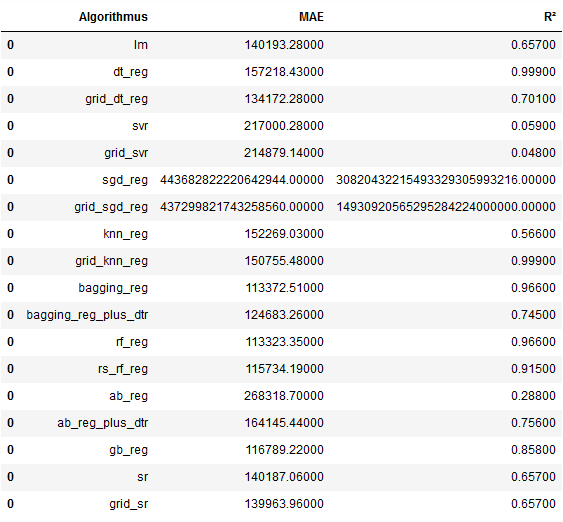

Now it is time to collect the calculated results.

column_names = ["Algorithmus", "MAE", "R²"]

df = pd.DataFrame(columns = column_names)

lm_df = pd.DataFrame([('lm', mae_lm, r_lm)], columns=column_names)

df = df.append(lm_df)

dt_reg_df = pd.DataFrame([('dt_reg', mae_dt_reg, r_dt_reg)], columns=column_names)

df = df.append(dt_reg_df)

grid_dt_reg_df = pd.DataFrame([('grid_dt_reg', mae_grid_dt_reg, r_grid_dt_reg)], columns=column_names)

df = df.append(grid_dt_reg_df)

svr_df = pd.DataFrame([('svr', mae_svr, r_svr)], columns=column_names)

df = df.append(svr_df)

grid_svr_df = pd.DataFrame([('grid_svr', mae_grid_svr, r_grid_svr)], columns=column_names)

df = df.append(grid_svr_df)

sgd_reg_df = pd.DataFrame([('sgd_reg', mae_sgd_reg, r_sgd_reg)], columns=column_names)

df = df.append(sgd_reg_df)

grid_sgd_reg_df = pd.DataFrame([('grid_sgd_reg', mae_grid_sgd_reg, r_grid_sgd_reg)], columns=column_names)

df = df.append(grid_sgd_reg_df)

knn_reg_df = pd.DataFrame([('knn_reg', mae_knn_reg, r_knn_reg)], columns=column_names)

df = df.append(knn_reg_df)

grid_knn_reg_df = pd.DataFrame([('grid_knn_reg', mae_grid_knn_reg, r_grid_knn_reg)], columns=column_names)

df = df.append(grid_knn_reg_df)

bagging_reg_df = pd.DataFrame([('bagging_reg', mae_bagging_reg, r_bagging_reg)], columns=column_names)

df = df.append(bagging_reg_df)

bagging_reg_plus_dtr_df = pd.DataFrame([('bagging_reg_plus_dtr', mae_bagging_reg_plus_dtr, r_bagging_reg_plus_dtr)], columns=column_names)

df = df.append(bagging_reg_plus_dtr_df)

rf_reg_df = pd.DataFrame([('rf_reg', mae_rf_reg, r_rf_reg)], columns=column_names)

df = df.append(rf_reg_df)

rs_rf_reg_df = pd.DataFrame([('rs_rf_reg', mae_rs_rf_reg, r_rs_rf_reg)], columns=column_names)

df = df.append(rs_rf_reg_df)

ab_reg_df = pd.DataFrame([('ab_reg', mae_ab_reg, r_ab_reg)], columns=column_names)

df = df.append(ab_reg_df)

ab_reg_plus_dtr_df = pd.DataFrame([('ab_reg_plus_dtr', mae_ab_reg_plus_dtr, r_ab_reg_plus_dtr)], columns=column_names)

df = df.append(ab_reg_plus_dtr_df)

gb_reg_df = pd.DataFrame([('gb_reg', mae_gb_reg, r_gb_reg)], columns=column_names)

df = df.append(gb_reg_df)

sr_df = pd.DataFrame([('sr', mae_sr, r_sr)], columns=column_names)

df = df.append(sr_df)

grid_sr_df = pd.DataFrame([('grid_sr', mae_grid_sr, r_grid_sr)], columns=column_names)

df = df.append(grid_sr_df)

df['MAE'] = np.round(df['MAE'], decimals=3)

df['R²'] = np.round(df['R²'], decimals=3)

df = df.rename(columns={'R²': 'R'})

df['R²'] = abs(df.R)

df = df.drop(columns=['R'])

df

Ok this overview is not really readable yet. We can do better:

pd.options.display.float_format = '{:.5f}'.format

df

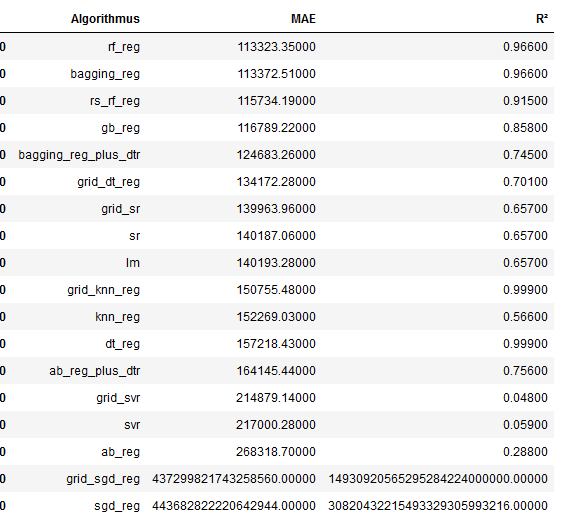

Now we display the MAE values in ascending order.

best_MAE = df.sort_values(by='MAE', ascending=True)

best_MAE

From the overview we can see that the RandomForestRegressor is the algorithm that achieved the best results.

pd.reset_option('display.float_format')What these metrics mean and how to interpret them I have described in the following post: Metrics for Regression Analysis

10 Conclusion

In this post I have shown which different machine learning algorithms are available to create regression models. The explanation of the exact functionality of the individual algorithms was not central. But I did explain them when I used these algorithms for classification problems. Have a look here: